What is a 401(k) Fiduciary: Key Responsibilities & Duties

If you help with the 401(k) plan, you are likely a 401(k) fiduciary. This remains true, even if the plan documents or the main administrator do not specifically mention you. If you're a 401(k) fiduciary and fail to act in your employee's best interests, you could face personal liability.

Whether you sign Form 5500 annually or handle part of the process, it's crucial to know your legal duties.

In this guide, we will explain everything you need to know about being a 401(k) fiduciary. This includes understanding your legal responsibilities and finding ways to reduce your liability and make compliance easier for your plan.

What is a 401(k) Fiduciary?

A 401(k) fiduciary is a person at a company who is responsible for managing the assets of the retirement plan. This responsibility includes most aspects of plan administration, as stated by the Department of Labor (DOL). It typically also includes anyone that renders investment advice.

Most likely, you’re a fiduciary if you…

- Sign the Form 5500 or other regulatory filings

- Sign plan documents, (like the Adoption Agreement) created by your TPA or recordkeeper

- Choose the retirement plan’s providers - or sit on the committee that hires plan providers

- Exercise authority over the plan - be it on the investment or administrative side

- Decide how to use plan assets for operating costs, such as administrative, investment advisory, or audit services.

- Have discretion over any area of plan management or help with plan administration

- Plan documents clearly identify you as a fiduciary, leaving no doubt that you are one.

If you do not meet the mentioned criteria, it is likely that you are not a fiduciary.

What It Means to Be a 401(k) Fiduciary

Fiduciaries are the people in charge of a 401(k) retirement plan. They have a legal responsibility to protect and take care of the participants' savings.

As you can imagine, fiduciaries are pretty important.

As a fiduciary, you’re legally responsible (and liable) for solely acting in your employee's best interest. That means mistakes, errors, or wrongdoing in managing your plan may ultimately be your responsibility. If the company doesn’t have the money to fix any errors, your personal assets may be on the hook.

The liability involved with being a fiduciary is serious, without a doubt. There are many ways to protect the plan sponsor, reduce liability, and meet fiduciary responsibilities.

By diligently documenting your oversight or retaining a qualified 401(k)advisor your fiduciary responsibilities do not need to be overwhelming.

401(k) Fiduciary Responsibilities

The 1974 Employee Retirement Income Security Act (ERISA) lays out the legal responsibilities of the fiduciary.

401(k) Fiduciary Plan Investment Responsibilities

Meeting investment responsibilities sounds pretty intimidating, but with time and expertise, they are relatively easy. When fulfilling your fiduciary duties, you must make sure that you adhere to two key principles:

- Duty of loyalty - act solely in the interests of participants and their beneficiaries

- Duty of care - exercise the care, skill and diligence of a prudent expert.

Pick Prudent Plan Investments

As the person managing investment, you have the responsibility to pick investments that meet plan objectives. You should routinely analyze each mutual fund's management, track record, expenses, risk, and performance. An investment policy statement can be a valuable guide.

ERISA defines the "prudent expert" rule as the standard for selecting and monitoring plan investments. It means that if you're responsible for someone's money, you must handle it wisely and try to make it grow.

Many index funds offer comparable returns and low fees and can be an excellent option.

Meet Diversification Requirements

To comply with ERISA Section 404(c) ERISA rules, you should provide various investment options and even education. This will allow employees to build diverse portfolios while managing a reasonable level of risk. An increasing number of plan sponsors are relying on registered investment advisors to help provide financial planning to their employees.

Review and Monitor the Investments

After selecting investments, you need to regularly check and track their performance and cost compared to similar investments with similar goals.

401(k) Fiduciary Plan Administration Duties

Ensure Compliance with Plan Design and IRS Rules

As the fiduciary, you are in charge of managing or supervising administrative tasks as outlined in the plan document. Plan rules you should pay special attention to include:

1. The Definition of Eligible Compensation

The type of compensation eligible for 401(k) deferrals (IE salary, wages, commissions, bonuses, etc).

2. Eligibility Requirements for Enrollment & Employer Contributions

You must naturally follow any age and service requirements defined in your plan document.

3. Deposits, loans, distributions, and QDROs

Ensure timely and accurate 401(k) contributions

401(k) payroll deferrals are the lifeblood of the 401(k). They’re how your employees’ money gets from your payroll system into the plan. And it’s your responsibility to make sure that happens smoothly. That means:

- Depositing contributions promptly.

- Ensuring that payroll correctly updates employee savings rates when employees change them on the 401(k) provider's website.

- Setting up loan repayments according to the repayment schedule provided by the 401(k) provider.

Send participants the required statements and notices

You must send participants certain notices at different times throughout the lifetime of your 401(k). We must send some every year, or every quarter. When a specific event happens, like when a new employee becomes eligible, you must send the right notices.

Keeping good records per the ERISA record retention requirements

Record retention is a huge part of dealing with a 401(k). During audits, auditors always request documents and records. It is important to be diligent and organized during these audits. This applies to both DOL and 401(k) audits.

Oversee annual compliance responsibilities

One important duty of a fiduciary is to supervise the yearly compliance work needed at the end of each plan year. This includes:

- Putting together the year-end census report.

- Conducting nondiscrimination testing and ensuring the correction of mistakes.

- Assisting with the annual 401(k) audit (if applicable).

- Preparing, signing, and submitting Form 5500.

401(k) Investment responsibilities

As a 401(k) fiduciary, your main role is to safeguard plan assets and ensure your employees have a secure retirement. To do this, you have to:

Ensure 401(k) fees are reasonable

The definition of "unreasonable expense" is unclear. However, the Department of Labor recommends that fees should align with the value of services offered.

Conducting annual or bi-annual fee benchmarking is a great starting point. Periodically soliciting competitive bids from leading 401(k) providers is even better. Just ensure you document these analyses to show you are meeting your fiduciary obligations. A knowledgeable investment advisor should be willing to perform this analysis on your behalf.

Fees taken from the plan can greatly decrease your savings if they become too high. These fees can be for fund expenses or administrative costs. So it’s your responsibility to ensure that they don’t.

Maintain fidelity bond coverage

As you handle other people's money, you need a "fidelity bond" insurance policy. This policy safeguards the 401(k) plan participants in the event of theft of plan assets.

In general, the plan assets must have a minimum coverage of 10% or $500,000, whichever is less.

Select and Oversee 401(k) Service Providers

Your main job is to select and oversee 401(k) service providers. If you decide to hire a fiduciary service provider, you can delegate tedious and time-consuming tasks to them. Additionally, they will also assume legal responsibility for meeting ERISA requirements.

However, the plan sponsor must ensure the plan fiduciary is doing their job correctly.

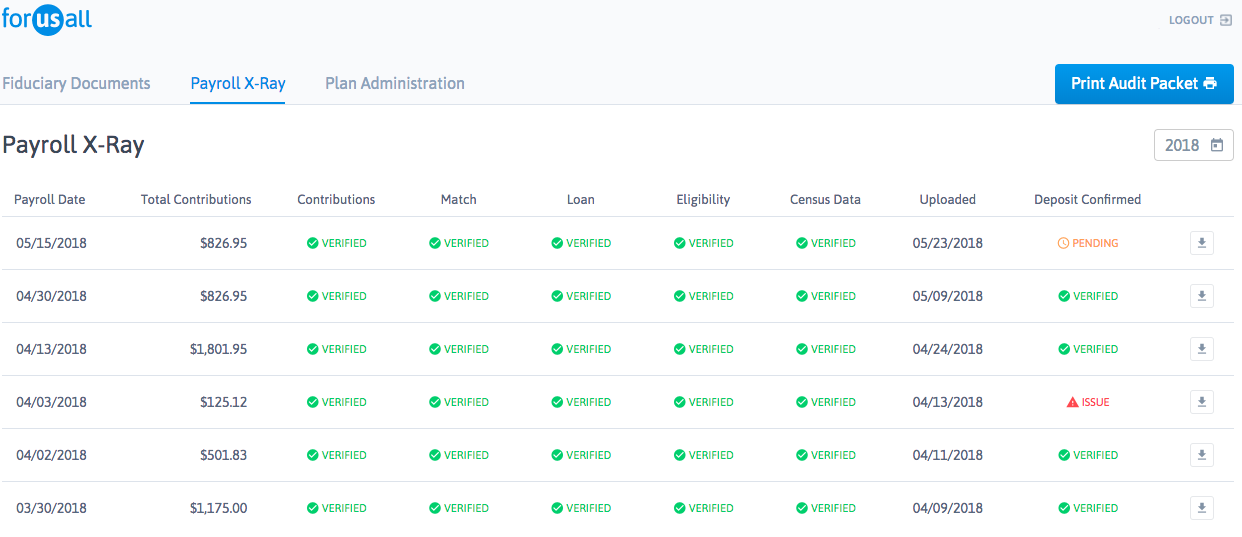

At ForUsAll, we’ve designed our platform to help make your oversight effortless. Employers are provided with a live dashboard. This dashboard allows them to view the mistakes we have found in their plan. Additionally, they can track the progress we are making to fix these mistakes.

Remember, no matter who you choose to help you out; the plan is ultimately your responsibility.

Types of 401(k) Fiduciary Service Providers

Luckily, ERISA does not require employers to shoulder all of their fiduciary responsibilities alone. In 2021, about 60% of 401(k) plan sponsors get assistance from an external consultant or advisor. Employers can reduce their fiduciary liability by hiring external fiduciaries. This is especially true after the 2022 Supreme Court decision, which raised the fiduciary standard.

3(21) & 3(38) Fiduciaries

Both 3(21) and 3(38) fiduciaries are financial advisors who choose and oversee investments for a plan.

In essence, the difference boils down how much responsibility (and liability) the investment advisor assumes. A 3(21) fiduciary will act as a “co-fiduciary,” and will advise and recommend funds for your lineup. However, the plan sponsor ultimately decides which investments to include.

By contrast, a 3(38) takes full responsibility for building, monitoring, and maintaining the plan’s fund lineup.

A 3(38) offers the highest level of fiduciary coverage related to investments.

3(16) Fiduciaries

A 3(16) fiduciary can help reduce workload and liability for administrative tasks. A 3(16) fiduciary is a 401(K) administrator responsible for:

- Overseeing the TPA work and results.

- Coordinating with the record keeper.

- Approving loans, rollovers, distributions & QDROs.

- Signing the Form 5500.

- Ensuring payroll deposits are accurate and timely.

- Interpreting plan documents.

- And much more..

The 3(16) takes over after the TPA and makes sure the daily administration follows the rules.

Conclusion

At ForUsAll, we believe that acting as a fiduciary is both a great responsibility and a greater privilege. As a fiduciary, you are responsible for ensuring your employee’s retirement savings are in good hands.

With that said, if 401(k) compliance and administration is something you’d rather not deal with, check out our solution! We do most of the work for your 401(k), reduce fees, and improve the experience for your employees.

The best part?

We offer 3(21), 3(38) and 3(16) fiduciary services, which allowing you to offload work and liability. Tour our solution today to learn more!